As of January 1, 2026, California has reinstituted asset limits for Medi‑Cal. This change affects many seniors, especially those who are already on Medi‑Cal or may need Medi‑Cal in the future for long‑term care, home health, or other services. If you’re on a fixed income or rely on Social Security and a small savings cushion, this rule could change how you plan for your health‑care costs and retirement savings.

What changed?

From 2024 to the end of 2025, many Medi‑Cal programs had no asset limits at all. You could apply without worrying about how much money you had in the bank, as long as your income met the rules. That “no‑limit” period was temporary.

Starting January 1, 2026, the old rules are back for most non‑MAGI Medi‑Cal programs (primarily for seniors and people with disabilities, including long‑term care):

- Single Californians may have up to $130,000 in countable assets.

- Married couples may have up to $195,000, with an extra $65,000 for each additional eligible household member, up to 10 people per household.

What counts as an “asset”?

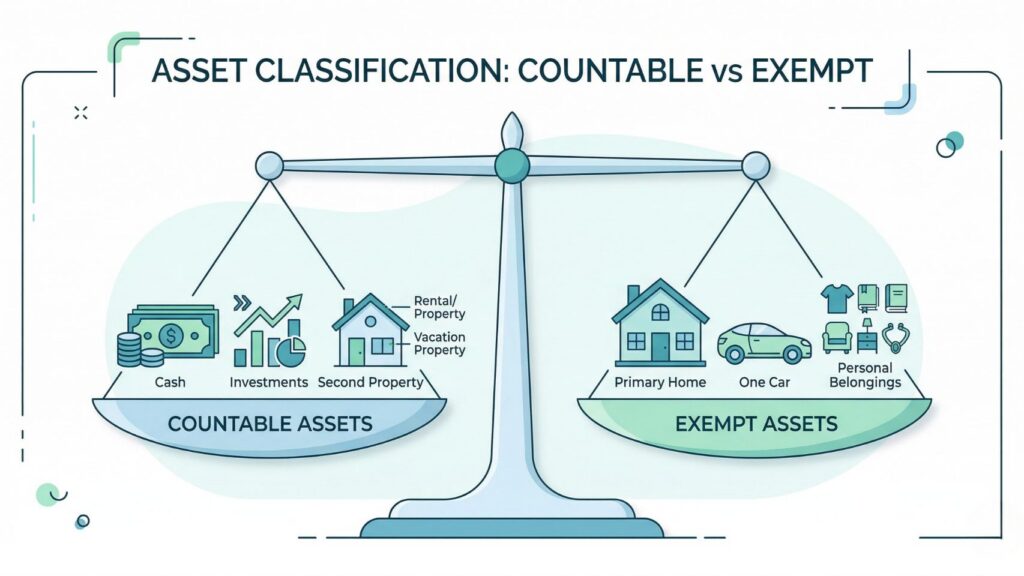

Medi‑Cal counts many kinds of money and investments, but not everything. Examples of countable assets include:

- Cash, checking and savings accounts

- Investment accounts (stocks, bonds, mutual funds, brokerage accounts)

- Promissory notes and cash‑surrender value of life insurance

- Second or extra cars, and investment or vacation real estate

Examples of usually exempt (not counted) assets:

- Your primary home (the house you live in)

- One personal vehicle

- Personal belongings, furniture, and household goods

- Certain retirement accounts, in many Medi‑Cal‑linked scenarios

Who is affected?

This change mainly touches people in two groups:

- Seniors already on Medi‑Cal

- If you get Medi‑Cal today, you’ll be asked to report your assets during your annual redetermination (the yearly check‑in).

- If you’re over the limit, Medi‑Cal will usually give you about 90 days to explain or reduce your assets before considering dropping your coverage.

- Seniors who may need Medi‑Cal in the future

- If you or a spouse may need nursing home care, in‑home aides, or other long‑term care in the next few years, you now need to think about your savings, investments, and transfers much more carefully.

- Large gifts, discounts, or sales of your home or assets may trigger a penalty period that stops Medi‑Cal from paying for care for months or even years.

Penalty rules you must know

California now uses a 30‑month “look‑back” period for transfers. That means:

- If you give away money or property, or sell it for less than fair market value, after January 1, 2026, Medi‑Cal can look back 30 months to see if you did so to qualify for help.

- If it finds you transferred assets to become eligible, it can impose a period of ineligibility during which you must pay for care yourself.

This is why it’s important to get legal or planning advice before making big gifts, selling a house cheaply to a family member, or pouring money into “gift annuities” or similar products.

So what should seniors do now?

Here are practical steps you can take today:

- Take a quick asset check

- List everything you own that could count toward Medi‑Cal: bank accounts, investments, extra cars, and investment property.

- Mark as “exempt” the items that usually don’t count, like your home and one car.

- If you’re near or above the limit

- Work with an elder‑law or Medi‑Cal‑planning attorney to look at strategies.

- There are legal ways to use your money to your benefit (paying down debt, necessary home repairs, pre‑paying burial, or buying an exempt asset) without losing coverage.

- Do not make a large gift or below‑market sale without professional advice; it can trigger a penalty.

- If you’re on SSI or SSI‑linked Medi‑Cal

- SSI has its own, stricter asset rules. Many SSI recipients lose benefits if they have more than about $2,000 in countable assets.

- Being under Medi‑Cal’s $130,000 asset limit does not mean you can safely exceed SSI’s much lower limit. Have a planner confirm your situation.

- If you may need long‑term care in the next 3–5 years

- Start an informal “Medi‑Cal readiness” plan.

- Ask: “Will I have more than about $130,000 in countable assets in a few years?”

- If the answer is yes, contact an elder‑law or Medi‑Cal‑planning professional now to design a plan that protects you and avoids look‑back penalties.

- If you are unsure, get an explanation

- Call your local Medi‑Cal office, your county Area Agency on Aging, or a Legal Aid / elder‑law clinic.

- Many organizations offer free or low‑cost Medicare/Medi‑Cal counseling and can help you understand your own numbers.

What this means for your peace of mind

For many seniors, this change is not a crisis, but it is a reminder: planning matters now more than ever. If you ignore it, you may find yourself unexpectedly disqualified from Medi‑Cal just when you need it most. If you pay attention and get help, you can usually stay within the rules while still protecting your lifestyle and legacy.

The bottom line: If you are 60 or older and depend on or may one day need Medi‑Cal, talk with a professional—an elder‑law or Medi‑Cal‑planning attorney or a certified elder‑care planner—about your assets, your goals, and the “penalty” rules. The earlier you plan, the more options you’ll have and the less stress you’ll face down the road.