Is your real estate agent acting as an unlicensed general contractor possibly creating a huge liability for you?

In California, it’s increasingly common for real estate agents to promise “concierge” or “project management” services—lining up painters, flooring installers, handymen, and other trades to get a listing market‑ready. That convenience can hide real legal and liability risks if the agent is effectively acting as an unlicensed general contractor and is not and cannot be properly insured.

How agents end up acting like contractors

Many listing agents now advertise that they will:

- Select and hire painters, flooring contractors, and other subs.

- Coordinate schedules, access, and scope of work.

- Approve changes, negotiate pricing, and “manage” the project for the seller.

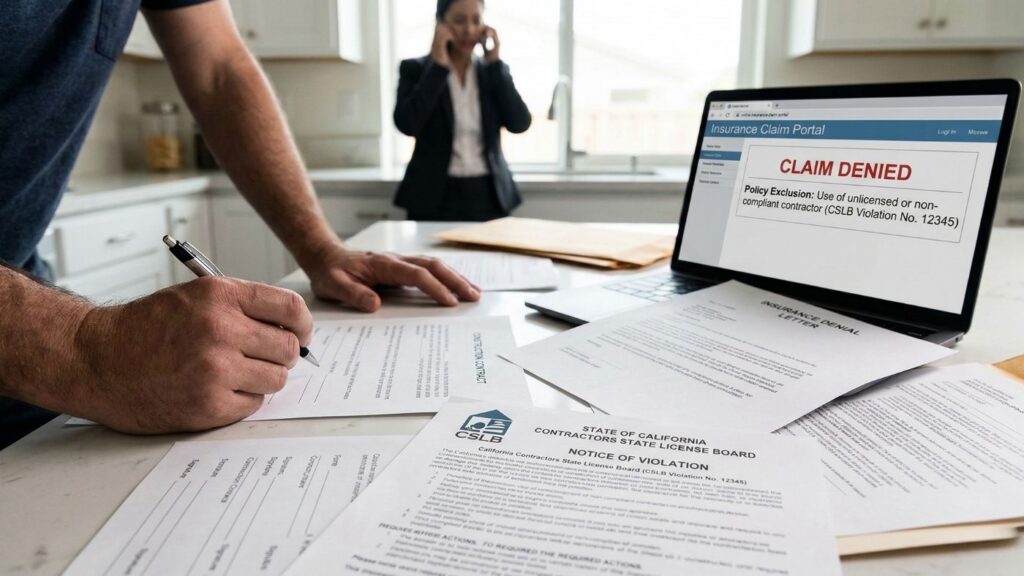

When an agent goes beyond simply referring a contractor and instead starts hiring or supervising multiple trades for a single improvement project, they can cross the line into acting as a contractor under California’s very broad Contractors’ State License Law (Business & Professions Code §7026, §7028, and related provisions). The law defines a contractor as anyone who “undertakes to” or “offers to undertake” construction, alteration, improvement, or repair work, directly or “by or through others.” That language is intentionally broad and can encompass an agent who organizes and controls subs performing construction work, even if the agent never swings a hammer.

Why hiring subs without a contractor’s license is a legal problem

Under California law, anyone who contracts for or manages construction work totaling $500 or more in labor and materials must hold an appropriate contractor’s license, unless a narrow exemption applies. Acting as an unlicensed contractor is not a minor technicality; it is illegal and carries consequences such as:

- The person cannot legally collect compensation for work that required a license.

- The Contractors State License Board (CSLB) can pursue administrative and, in some cases, criminal penalties.

- Courts can order disgorgement of all compensation tied to work done while unlicensed, which raises questions about whether a commission is at risk if part of the agent’s service package was unlicensed contracting activity.

A real estate broker license does not automatically authorize a licensee to act as a general contractor. There is a narrow “broker exemption” when the broker is acting strictly within the scope of real estate brokerage (for example, negotiating a purchase contract that incidentally involves repairs), but that exemption is not a free pass to manage full-blown renovation projects, hire multiple subs, or represent oneself as overseeing construction.

Insurance gaps: liability and workers’ compensation

When a true general contractor manages a project, that contractor typically has:

- General liability insurance, to respond to property damage or bodily injury claims arising from the work.

- Workers’ compensation insurance, to cover employees’ work‑related injuries.

By contrast, most real estate agents and brokers carry:

- Errors and omissions (E&O) coverage focused on professional negligence in brokerage, not construction defects.

- Sometimes a general liability policy for their brokerage premises and business activities, but not tailored to construction management.

Key issues for sellers:

- Injured worker on your property

- Many “subs” that agents use are one‑person operations or small crews with no workers’ compensation coverage.

- If a worker is hurt on your property and does not have their own workers’ comp, the law can treat the hiring party—or even the property owner—as the “statutory employer.” That can expose the homeowner to workers’ compensation liability or civil lawsuits for medical costs and lost wages.

- If the agent is functioning as an unlicensed contractor and has no workers’ comp policy, there may be no insurance “backstop” between you and the injured worker’s claim.

- Property damage caused by an uninsured sub

- If an uninsured painter or floor installer causes a fire, flood, or major damage, you will look first to:

- The sub’s liability insurance (often nonexistent or minimal).

- The general contractor’s liability policy.

- Your own homeowner’s policy, which may or may not fully respond depending on policy language about “business” or “construction” risks.

- If your agent was acting like a general contractor but has no contractor’s liability policy, there is a real risk that neither their E&O policy nor their brokerage GL will cover construction‑related damage. An insurer can argue that construction management falls outside the professional real estate services the policy was underwritten for.

- If an uninsured painter or floor installer causes a fire, flood, or major damage, you will look first to:

In short, when an agent acts as a de‑facto GC without the proper license and insurance, the liability “triangle” (owner–GC–subs) is broken, and the homeowner may be the deepest pocket in the chain.

Legal and financial risks to the seller

Allowing an agent to run the project as an unlicensed, uninsured GC can create several layers of exposure for a home seller:

- Regulatory risk: If a dispute arises and a court finds the agent was acting as an unlicensed contractor, the agent may be barred from collecting some or all compensation tied to the transaction, and the situation can draw CSLB scrutiny. That can drag the seller into a mess of depositions and enforcement actions.

- Contract enforceability: Contracts made with unlicensed contractors can be void or voidable, and disputes over payment to subs can result in liens, stop notices, or litigation that complicate or delay your sale.

- Direct financial liability:

- Work‑injury claims from laborers who are treated as your “employees” because no one else in the chain carried workers’ comp.

- Costs to repair shoddy or damaging work when there is no solvent or insured contractor standing behind it.

- Potential non‑covered claims under your homeowner’s policy if the carrier says the risk should have been placed under a contractor’s policy.

Why hiring an agent who is also a licensed and insured GC is safer

If you want “one‑stop” handling of pre‑sale improvements, the safer arrangement is to work only with real estate professionals who are also properly licensed and insured general contractors (or who bring in a separate licensed GC to take responsibility for the work). That means:

- A valid California contractor’s license in good standing in the name of the person or entity actually contracting for and managing the work.

- Active general liability coverage that specifically covers contracting operations.

- Workers’ compensation insurance in place if there are any employees, with confirmation of coverage for all subs or a requirement that subs provide their own certificates.

Benefits to the seller when the person managing the work is a true GC (even if they also hold a real estate license):

- Proper risk allocation: The GC’s insurance is designed to sit in front of your homeowner’s policy for construction‑related injuries and property damage, significantly reducing your personal exposure.

- Better leverage in disputes: If there is defective work or unpaid subs, you have a regulated, licensed party with bonding and insurance requirements to pursue.

Practical tips for California home sellers

If your listing agent offers to “manage” upgrades, ask:

- Are you acting as a general contractor on this project, or simply referring me to licensed contractors I will hire directly?

- Do you (or your entity) hold a current California contractor’s license? In what classification?

- Do you carry general liability insurance specifically for contracting activities? At what limits?

- Do you have workers’ compensation coverage, and will you verify coverage or certificates of insurance for all subs working on my property?

If the honest answer is that the agent is not a licensed contractor and does not carry contractor‑grade insurance, a cautious seller should either:

- Hire a separate licensed and insured general contractor to manage the work, or

- Limit the agent’s role to referring reputable contractors, leaving the contracting relationship directly between you and the licensed GC.

Framed this way, the question isn’t whether an agent can “help with upgrades” in California—it’s whether they are doing so in a way that complies with contractor licensing laws and preserves the liability protections that sellers reasonably expect. Only allowing a real estate agent who is also a properly licensed and insured general contractor to manage upgrades is often the more legally defensible and financially prudent choice.

Vabrato Inc (DRE# 02142060) is a Bay Area real estate brokerage that manages and performs upgrades on homes for sellers. Its broker is a California licensed general contractor that is bonded and carries both liability and workers comp insurance, so their clients are protected from liability.